For companies engaged in European import business, the term “VAT Deferral” is probably no stranger. It is often hailed as a magic tool for relieving financial pressure, but its operating mechanism, applicable conditions, and potential risks are not well known to everyone. This article will systematically break it down to help you judge whether your company is suitable for this policy.

What is VAT Deferral?

VAT deferral is a customs tax collection policy. When goods are imported into the EU, the import VAT that should be paid immediately can be deferred until the goods are actually sold.

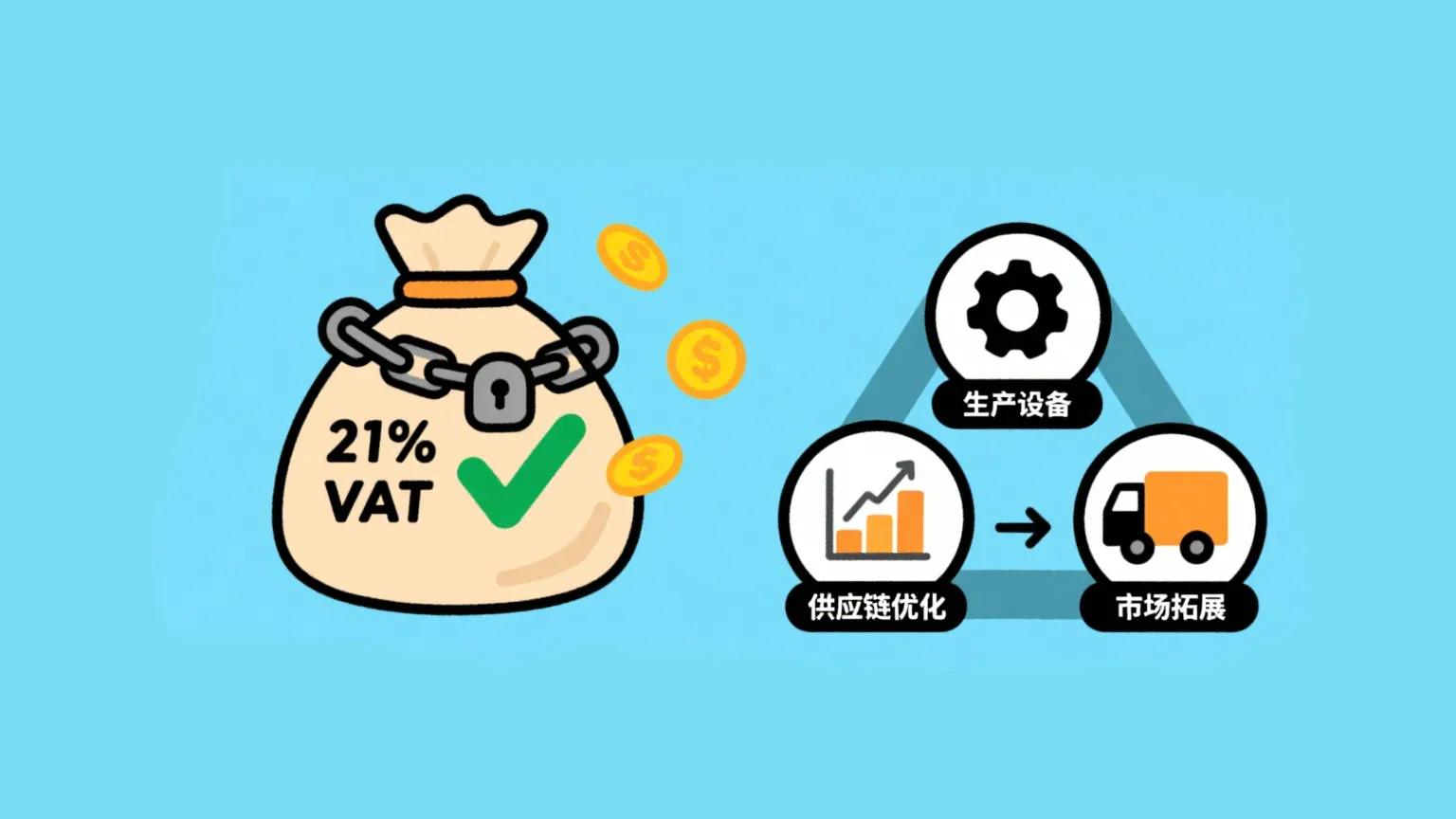

EU countries have different tax rates, for example Spain is 21%, Italy is 22%, Germany is 19%. This means that for a high-value goods at import, the VAT amount could be considerable. The deferral policy allows companies to keep the funds that would have been paid in advance in their hands, greatly improving cash flow and reducing capital occupation.

How to Apply and Operate? Who is Eligible?

Obtaining VAT deferral qualification is not automatic, but is achieved based on the company’s specific situation, mainly through the following three ways. Companies must have a valid VAT tax number and meet corresponding compliance requirements.

Three Ways to Obtain Deferral Qualification:

Method 1: Automatically Obtain When Revenue Reaches Standard

When a company’s annual revenue exceeds a specific standard (for example, Spain is €6,010,121.04), the tax authority will mandatory require it to switch to monthly VAT declaration. Once included in this category, the company will automatically obtain VAT deferral qualification.

Method 2: Proactive Application Approval

For the vast majority of small and medium-sized enterprises that do not meet the above revenue standard, they need to actively submit an application to the tax authority during November 1-30 of the previous year (for example, Spain’s AEAT 036 form). After approval, they can officially obtain deferral qualification on January 1 of the following year.

Method 3: New Company Special Application

Newly registered companies can also apply for deferral qualification directly at the time of establishment. If approved during the registration phase, the company will have the relevant qualification from the beginning of operations.

Qualification Verification and Operation Process:

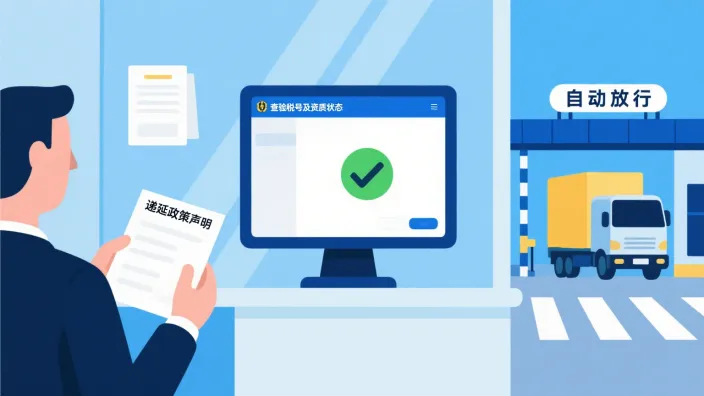

Regardless of how qualification is obtained, in actual operation, when goods are declared for import, the company needs to declare to customs that it will use the deferral policy. Customs staff will verify the company’s tax number and qualification status in real time through the system. If the system shows that the qualification is valid and the company has no tax violations, customs will automatically accept the deferral application and release it without requiring the company to pay VAT on the spot.

What Are the Benefits and Potential Risks?

Advantage: Effectively Liberate Cash Flow:

No need to pay VAT up to 21% of the goods value at import, funds can be used for more core business links.

Risk: Higher Compliance Requirements and Potential Costs:

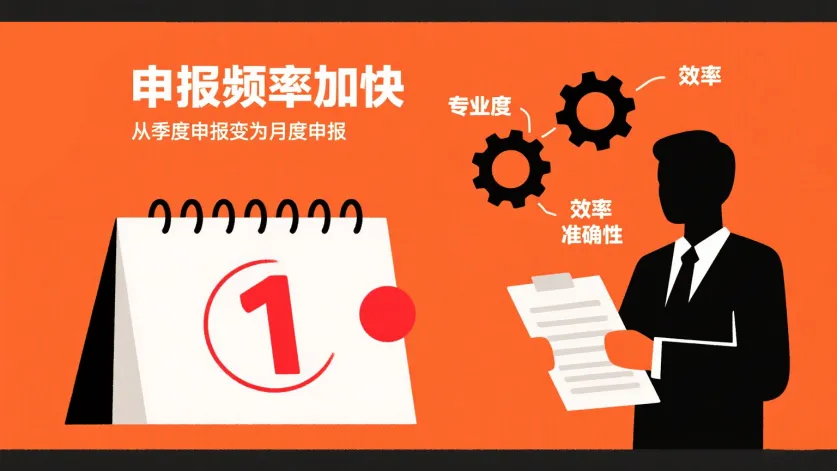

Faster declaration frequency: After applying for deferral qualification, the company’s VAT declaration cycle will usually change from quarterly declaration to monthly declaration, which puts forward higher requirements for the professionalism and efficiency of financial personnel.

Stricter tax supervision:

Since the company essentially “owes” the tax authority money, it will become a focus object of the tax department, and the probability of being checked and audited may increase. This requires companies to maintain clear and compliant accounts, and rely on professional and reliable accounting or law firms.

Not applicable to all situations: For companies that import low-value and sell high value-added products, the cash flow benefits brought by deferral may not offset the tediousness and pressure of monthly declaration and immediate payment of sales VAT.

Important Notes and Common Misconceptions

Misconception: Customs Manages Deferral?

No. Customs is only responsible for collection and release on behalf. The real approval and management of deferral qualification is the tax authority. Customs at the import link only checks the company’s qualification status in the tax authority system.

Note: Compliance is the Lifeline

Even with qualification, compliance cannot be less. If the company has historical tax arrears, especially if last month’s payable tax is not paid, the tax authority will immediately synchronize the information to customs, resulting in the rejection of the current deferral application.

Warning: Don’t Be Speculative

Never try to use the deferral policy to evade taxes. Europe attaches great importance to integrity. Once there is a violation record, the company will face serious consequences such as higher inspection rates and blocked clearance. In the long run, the loss outweighs the gain. Only compliant operation can continue to enjoy policy dividends.

Although the VAT deferral policy is good, it is not suitable for all companies. It’s like a professional financial tool. When used correctly, it can greatly improve capital efficiency, but if used improperly or with a lucky mentality, it will trigger serious compliance risks. In recent years, we have witnessed many cases attempting to use policy loopholes, ultimately leading to account freezing, soaring inspection rates, and even legal prosecution, with costs far beyond imagination.

The European tax system attaches great importance to corporate integrity, and compliance is always the cornerstone of cross-border trade. We strongly recommend that you: before taking action, be sure to conduct a comprehensive assessment based on your own business model, financial ability, and sales channels. If you have doubts about your own qualifications, or want to know how to compliantly apply for and use the deferral policy, welcome to contact us MYU at any time.